As government support measures related to the pandemic have ended almost everywhere, we expect insolvencies to rise sharply in some major markets.

Summary

- Sharp insolvency increases in some major economies in 2022 and 2023.

- This is due to a weaker economic outlook with high inflation and energy prices and monetary tightening and the expiry of government support.

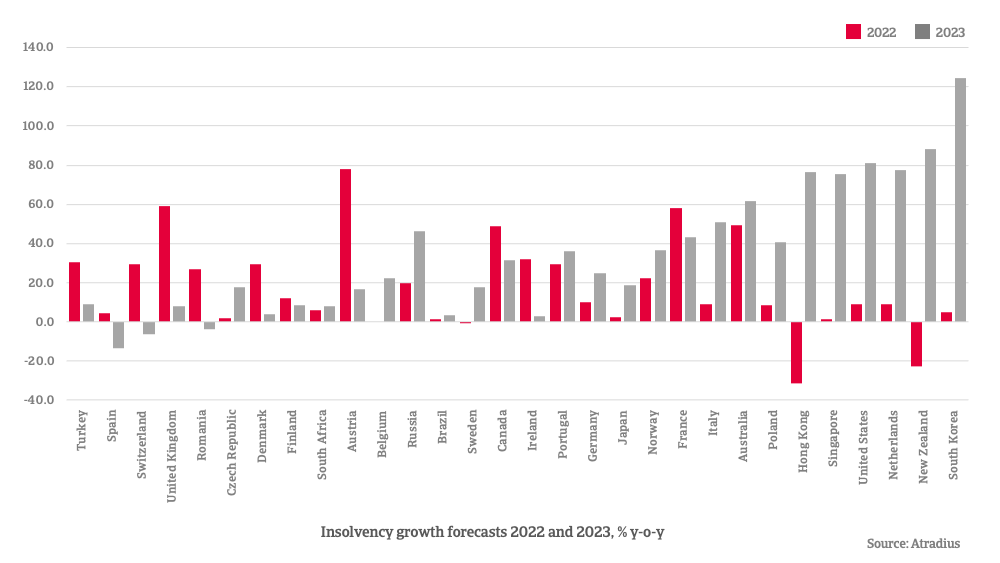

- In 2022, we expect sharply rising business failures in the United Kingdom (59%), France (58%), Austria (78%), Belgium, Canada and Australia (each 49%)

- In 2023, we forecast major increases in the United States (81%), the Netherlands (77%), Singapore (76%) and Italy (51%)

- For many markets we forecast an overshooting of normal levels of insolvencies in 2023 – a result of additional defaults of ‘zombie companies’.

Global economic woes persist

The economic outlook has continued to weaken in the past six months, with high inflation and high energy prices as the main culprit. We now forecast 2.9% growth for the global economy in 2022, followed by 1.7% in 2023. This is a cumulative 2.0 percentage point reduction up to 2023 compared to our April 2022 Insolvency Forecast report.

Energy prices have increased more than expected, given Russia’s further cuts to gas exports. There are signs that supply chain pressures are beginning to ease. Bottlenecks will continue to disrupt activity, but constraints on production should slowly ease. High inflation forces central banks to tighten monetary policy. For 2022 we forecast an average inflation of 7.8% globally, followed by 4.8% in 2023. Even though recession fears are growing, the stickiness of inflation will keep central banks cautious to ease monetary policy in the near term.

Tighter financial conditions in emerging markets

Emerging markets as a group are forecast to grow by 3.5% in 2022 and 3.4% in 2023. Covid-19 outbreaks and lengthened lockdowns weigh on growth in Emerging Asia. Additionally, EMEs increasingly face tighter financial conditions as central banks in advanced markets raise interest rates in response to higher inflation. Growth in Emerging Asia continues to moderate, though it remains the fastest growing region in 2022 (+3.8%).

In China, economic activity is expected to slow from 8.1% in 2021 to 3.2% in 2022 and 4.9% in 2023. Covid restrictions continue to affect activity, though authorities have fine-tuned the zero-Covid policy to reduce supply-side disruptions caused by lockdowns. China’s important real estate sector is in a downturn, and developer defaults remain the biggest risk to the outlook.

In Eastern Europe, the outlook continues to be dominated in the near term by the Russia-Ukraine war. Western countries have imposed massive sanctions on Russia, which pushes the Russian economy into recession both in 2022 and 2023. Turkey’s economy is facing a growth slowdown as inflation has risen steeply, biting into consumers’ purchasing power, and the global backdrop is worsening.

Advanced economies’ growth to slide to 2.3% in 2022 and 0.3% in 2023

Growth in the advanced economies is projected to slide from 5.2% in 2021, to 2.3% in 2022 and 0.3% in 2023. The United States economy had a weak start of the year, with two consecutive quarters of GDP decline. Rising inflation is biting into consumers’ real incomes, reducing domestic demand. For 2022 we expect 1.7% growth in the US, followed by 0.0% in 2023. Eurozone GDP growth was resilient in Q1 and Q2, as domestic demand expanded on a reopening of the services sector and a booming tourism sector. For the second half of the year and beginning of 2023, we expect the eurozone economy to enter a recession, mainly as a result of much higher energy prices. The main impact of the Russia-Ukraine conflict will be via higher commodity prices and disruptions to supplies of key imports such as gas from Russia and Ukraine. We forecast 3.0% eurozone growth in 2022, followed by 0.0% in 2023. For 2023, this is a 2.7 ppts downward adjustment compared to our April 2022 Insolvency Forecast report.

Aggressive monetary tightening makes financing harder

While government fiscal support related to the pandemic will weaken in 2022 compared to 2021, the overall fiscal position continues to be expansionary in most advanced markets. Against a backdrop of high inflation, central banks tighten monetary policy further.

- The US Federal Reserve raised its target policy rate by a cumulative 300 basis points so far in 2022, with three historic 75 bps hikes in June, July and September.

- Likewise, the Bank of England also implemented several rate hikes this year.

- The ECB hiked the policy rate by 50 bps in July and by another 75 bps in September, lifting the deposit rate to 0.75%, the highest level in over ten years.

We expect the central banks of major advanced markets to further hike policy rates in the coming quarters. Financial conditions have tightened both in advanced markets and EMEs. In most EMEs, they are already quite restrictive compared to historical norms, which could become a problem for markets with high company debts (e.g. Turkey).

Current level of insolvencies – partial adjustment to pre-pandemic levels after decreases in 2020

During the Covid-19 pandemic, we witnessed a strong decline of insolvencies (globally insolvencies fell by a cumulative 29% in 2020-2021). We have argued before that two types of policies are responsible for this development. First, most countries made (often temporary) changes to their insolvency legislation in order to protect companies from going bankrupt. Second, governments across the world took measures to counter pandemic-related adverse economic effects, including support for small businesses.

Decline in insolvencies in 2020 and 2021

In 2020 we saw that in virtually all markets there was a decline in insolvencies, despite the severe economic downturn. This was the effect of generous government support that saved not only viable companies, but also created zombie companies, i.e. companies that would have defaulted in normal times. In 2021 we already saw a partial adjustment to normal, pre-pandemic insolvency levels, a process that continued in the first half of 2022. This coincided with the phasing out of government support programmes. At the start of the third quarter of 2022, support programmes are phased out in all countries, except New Zealand and Hong Kong.

2022 year-to-date insolvency levels compared to 2019

Chart 1 gives the year-to-date insolvencies index in 2022 relative to the same period in 2019. This shows where the current level of insolvencies is standing in comparison to the pre-pandemic situation. The index shows a wide variation between countries, with some countries already above the 2019 level, while others continue to have very low insolvency levels.

Why are insolvency levels per countries still different?

Countries with a full reversal or that are overshooting pre-pandemic insolvency levels are Turkey, Spain, Switzerland, the United Kingdom, Czech Republic, Romania and Denmark.

In Spain, the adjustment to normal already took place in 2021. The economic recovery was disappointing and we think an ineffective legislative framework regarding restructuring and insolvencies contributed as well. In June 2022, the Spanish congress passed a new insolvency law based on the EU directive in insolvency, but it is unclear yet what impact this will have.

In the United Kingdom, the insolvency level is well above the pre-pandemic level. This can be attributed to ending of government support measures and the weak economic recovery since Brexit.

By contrast, in the Netherlands, United States, South Korea and Japan we do not yet see a reversal to normal levels. Even in recent quarters, insolvency levels in these countries remained very low. These countries all had relatively generous government support programmes that have improved the liquidity position of firms. The United States had business liquidity support programmes such as the Paycheck Protection Program available until the first part of 2021 and the Covid-19 Economic Injury Disaster Loan offered until end of 2021.

The Netherlands had several company support packages (e.g. NOW, TVL, Tozo) that have boosted companies’ liquidity. Moreover, a new insolvency law was effective from January 1st 2021. According to data, however, this law did not make a material contribution to lowering insolvencies. In Japan, there was also generous government support. We found evidence that there was a large increase in cash and deposits of non-financial corporations which may very well suppressed insolvency growth. South Korea also still has a relatively low insolvency level, which is attributed to corona support measures, including the availability of low-interest loans.

2022 and 2023: a continuation of the adjustment to normal and additional defaults from zombies

We are convinced that most countries will see their insolvency levels return to normal once support is discontinued. We quantify the normal level of insolvencies at a given point in time on the forecasting horizon by taking as a benchmark the insolvency counts in 2019 and adjusting this with the effect of the change in GDP deviation from trend relative to 2019.

The speed at which this normalisation takes place is assumed to be more gradual than in our previous Insolvency Forecast report. We expect it can take up to eight quarters after government support is discontinued before the insolvency level reaches the normality level. In our previous report, this was generally assumed to be two quarters.

On top of the normalisation, we distribute on the forecasting horizon additional defaults coming from zombie companies. Zombie companies are likely to occur because in the pandemic period the insolvency levels contracted well below their pre-pandemic levels. We believe that these companies will gradually default after the government support is withdrawn.

Additional defaults from zombie companies

We now turn to our insolvency forecast for 2022 and 2023, which is given in year-on-year % changes (e.g. 2022 compared with 2021). For the majority of countries, government support was phased out in the first half of 2022. Therefore, we see the adjustment to normal insolvency levels starting to take place in the second half of 2022.

We see that, in general, 2022 year-on-year growth rates are higher for countries that have already begun to adjust to normal and where zombie defaults occurred. If countries come from a low insolvency level in 2021, this gives further upward pressure to the forecast for 2022, as the adjustment is taking place in relatively large steps. In general, countries with high growth rates in 2022 experience low growth rates in 2023 and vice-versa.

War in Ukraine and insolvencies: biggest impact felt in Russia

Besides the effect on insolvencies following from the discontinuation of government support, another driver of insolvency growth is the change in GDP. By taking this into account, we include indirectly a broad range of factors affecting the economic outlook, such as high inflation, supply disruptions and the Russia-Ukraine conflict.

Apart from Ukraine, for which we do not have insolvency statistics, Russia will feel the biggest impact of the war, with its economy plunged into recession this year and in 2023. In other markets, the conflict is mostly felt indirectly, though higher commodity prices and high inflation, biting into consumers’ purchasing power and lowering GDP growth. For the eurozone, GDP impact of the Russia-Ukraine war is significant, as it is relatively dependent on energy imports from Russia. However, in many other regions outside Europe, such as Latin America, the impact of the Russia-Ukraine war on GDP and insolvencies is relatively small.

2022: high insolvency rates in markets where fiscal support was phased out

We present in Chart 2 the 2022 and 2023 year-on-year growth rates for all the markets in our analysis arranged in the same order as Chart 1.

The highest rates for 2022 are recorded in Austria, United Kingdom, France, Australia, Canada and Belgium, countries that have already adjusted partially or fully to their pre-pandemic insolvency levels. Fiscal support in these countries was phased out in the first half of 2022 and the adjustment to normal has already started and will continue in the second half of 2022.

On the other side of the spectrum, in New Zealand and Hong Kong we see a substantial decrease of insolvencies in 2022. This is because in their case the fiscal support is expected to extend until the end of 2022. There is a sizable group with slightly negative (Sweden) or mild positive insolvency growth (Singapore, South Korea, Japan, United States, Czech Republic and Spain).

Sweden has an erratic pattern of insolvencies and these did not decline very strongly during the pandemic, which explains why it is not seeing positive insolvency growth in 2022. In Singapore, insolvencies declined in 2020 and reverted back to higher levels in 2021. In Q3 2022 insolvencies surprisingly declined, which drags down yearly growth in 2022. Spain and Czech Republic already experienced a return to normal in 2021, which limits growth in 2022.

The United States, Netherlands, Japan and South Korea seem to benefit from relatively generous support measures that increased firms’ liquidity as much as to offer a buffer even after these measures are phased out.

Insolvencies in 2023: overshooting of normal levels in many markets due to more defaults of zombie companies

We note that the 2023 growth rate is highest in South Korea, New Zealand, the United States, Hong Kong, Singapore and the Netherlands, all countries with negative or only mild insolvency growth in 2022. For these countries, the adjustment to normal takes place largely in 2023.

For New Zealand and Hong Kong, fiscal support is expected to be phased out by the end of 2022. This concentrates all the adjustment in 2023, inflating the growth rate of insolvencies. For the United States, the Netherlands, South Korea and Singapore, government support already ended, but was arguably generous enough to prevent many insolvencies in 2022, as we explained in the previous paragraph. For these countries, we also forecast that the adjustment back to normal insolvency levels largely takes place in 2023. For many of the observed markets, we forecast an overshooting of the normal level of insolvencies in 2023. This is the result of additional defaults coming from zombie companies.

More troubles ahead for highly leveraged businesses

Beyond 2023, we expect that insolvencies will again start to decline or remain approximately constant. This is because insolvency levels will have largely returned to normal and zombie firms that are not able to survive without support, have gone bankrupt already. In the coming years, firms will have to adjust to an environment without significant government support. For firms that have taken up a lot of debt during the pandemic, this could be a challenge.

Theo Smid, Senior Economist

theo.smid@atradius.com

+31 20 553 2169

Learn more here: https://atradius.ca/reports/economic-research-sharp-increase-in-insolvencies-as-government-support-expires.html